The Advanced Driver Assistance Systems (ADAS) market is experiencing significant growth and transformation, driven by advancements in integrator platforms, simulation technologies, sensors, processors, and software. The market size for ADAS is projected to reach US$81.17 billion by 2032, representing ~ 18.2% CAGR (2023 – 2032). The ADAS market encompasses various systems and components that are integrated into vehicles to assist drivers. These systems rely on automated technology, including sensors, detectors, and high-resolution cameras, to monitor the surrounding environment and take appropriate actions.

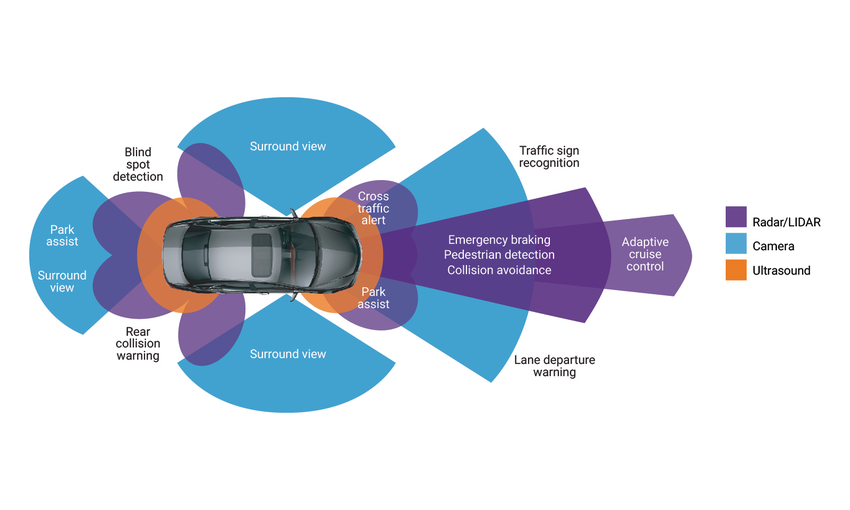

In this post, we will delve into key insights regarding major areas of the ADAS market, with a specific focus on the sensor segment, which is further sub-segmented into cameras, 4D radar, and LiDAR.

Based on consumer interest and the current market availability of AD features, McKinsey analysis suggests that ADAS and AD could generate between US $300 billion and US$400 billion in the passenger car market by 2035. The potential of AD goes beyond consumer benefits; it has the power to transform the automotive industry and reshape the way we perceive and utilize transportation. This technological shift places greater importance on automotive sensors, leading to the rapid adoption of new sensor products such as LiDAR, 4D imaging radar, and CMOS image sensors (CIS) in vehicles, etc. As a result, there is a growing demand for sensor chips, and automotive sensor and chip technologies are experiencing rapid iterative evolution and cost reduction.

Based on consumer interest and the current market availability of AD features, McKinsey analysis suggests that ADAS and AD could generate between US $300 billion and US$400 billion in the passenger car market by 2035. The potential of AD goes beyond consumer benefits; it has the power to transform the automotive industry and reshape the way we perceive and utilize transportation. This technological shift places greater importance on automotive sensors, leading to the rapid adoption of new sensor products such as LiDAR, 4D imaging radar, and CMOS image sensors (CIS) in vehicles, etc. As a result, there is a growing demand for sensor chips, and automotive sensor and chip technologies are experiencing rapid iterative evolution and cost reduction.

Camera sensors have established themselves as a mature industry within the ADAS market. They are widely adopted in vehicles for various applications, including lane departure warning, traffic sign recognition, and pedestrian detection. The competition landscape for camera sensors is relatively stable, with multiple established players providing reliable and cost-effective solutions.

On the other hand, 4D radar, an upgraded version of traditional millimeter-wave radar, is an emerging technology with immense potential in the ADAS market. Unlike traditional radar, 4D radar can process height information along with its original functions, providing enhanced capabilities for object detection and tracking. Currently, most L2+ ADAS systems employ traditional millimeter-wave radar, while 4D radar is not yet broadly utilized. However, it is expected to gain traction in L3 autonomous vehicles due to its advanced features.

One of the critical factors for success in the 4D radar segment is the ability to provide high-resolution radar techniques that outperform traditional radar solutions. This improvement allows for more accurate object detection and tracking, which is crucial for ADAS and autonomous driving systems.

Additionally, a cost-effective approach is paramount for the widespread adoption of 4D radar technology. Single System-on-Chip (SoC) solutions are considered a promising path to achieve cost-effectiveness, as they integrate multiple functionalities into a single chip. By reducing the overall system complexity and costs, single SoC solutions have the potential to accelerate the adoption of 4D radar in the market.

In addition to cameras and 4D radar, LiDAR technology is also an important component in the ADAS market. However, there are a few considerations specific to the LiDAR market. Firstly, LiDAR systems are generally more expensive compared to other sensor technologies, which can be a barrier to their widespread adoption. Additionally, the competition landscape in the LiDAR market is relatively stable, with two top players, Hesai and Robosense, dominating the market. These established companies have already demonstrated mass production capabilities and are working towards reducing costs. As a result, it may be challenging for new startups to enter the LiDAR market and compete effectively.

As the ADAS market continues to evolve, collaboration among sensor manufacturers, integrators, and software developers is crucial for the seamless integration and optimization of ADAS functionalities.

Updates from GLy’s Ecosystem

We are excited to celebrate the success in our portfolio and to share the recent news of Ascend Elements. The company has secured a multi-year contract worth up to $5 billion to supply sustainable precursor cathode active material (pCAM) for a major U.S. battery manufacturer, marking a significant shift in worldwide battery material supply chains. Ascend Elements’s continued commitment to building one of North America’s first commercial-scale NMC pCAM manufacturing facilities in Kentucky showcases their dedication to manufacturing critical battery materials domestically, reducing carbon emissions, and ensuring energy independence.

Investing in Ascend Elements offers several merits in the industry. The company’s innovative approach addresses the increasing demand for battery recycling, contributing to the shift towards electric vehicles and environmental sustainability. Ascend Elements’ well-funded status and partnerships with industry leaders such as SK Battery America, Jaguar Land Rover, and Honda position it as one of the most promising battery recycling startups in the US, well-equipped to tackle the emerging challenges in the domestic supply chain. Furthermore, its diversified product offering provides flexibility in capturing market opportunities as the value chain and recycling ecosystem evolve.

Ascend Elements’ successful fundraising efforts indicate the confidence in their innovative solutions and long-term market viability, and the team has continued to solidify their position as a frontrunner in sustainable battery material production.

We are proud to be a part of Ascend Elements’ journey and look forward to witnessing their continued success as they contribute to the advancement of the battery industry and the overall energy transition.

Read more here: Ascend Elements to Supply Sustainable Cathode Precursor (pCAM) Made from Recycled Battery Materials to Major U.S. Customer. This deal marks a significant shift in battery material supply chains and aims to enhance North America’s energy independence while reducing carbon emissions.

Polestar

Starting in 2025, new Polestar vehicles in North America will come with the Tesla-designed NACS plug, while existing Polestar owners can charge at Tesla’s Supercharger stations with an adapter by mid-2024. This move aligns Polestar with other major automakers like Volvo, Ford, General Motors, and Rivian, who have also entered similar agreements with Tesla recently.

Polestar announced a joint venture with Xingji Meizu, a Chinese mobile phone and consumer electronics company, to develop a customized operating system for Polestar cars sold in China. The JV aims to integrate Xingji Meizu’s Flyme Auto OS into Polestar vehicles, offering a tailored user experience for the Chinese market, including in-car apps, streaming services, and intelligent vehicle software.

Geely Auto Group has launched the Geely Galaxy L7, its first model in the new Galaxy electric vehicle lineup, as part of its strategy to compete with BYD and Tesla in China’s electric vehicle market. The compact SUV offers two battery range option, with a CLTC pure electric range of 55 km and 115 km, as well as a combined range of up to 1,370 km on full fuel and full charge. The new model features advanced technologies such as the Aegis battery safety system and the NordThor Hybrid 8848 powertrain. With plans to release up to seven models in the Galaxy lineup by 2025, Geely aims to establish itself as a major player in China’s growing electric vehicle sector. The launch of the Geely Galaxy series marks Geely Auto’s commitment to the electrification of its vehicle lineup and its goal of selling at least 600,000 electrified cars in 2023.

Aston Martin to partner with Lucid Group with developing EV performance powertrain, battery modules and software for Aston Martin’s ultra-luxury high-performance EV. This collaboration supports Aston Martin’s electrification strategy, aiming to offer electrified powertrain options across their vehicle lineup by 2026 and achieve full electrification by 2030.

Zeekr has started accepting pre-orders for its luxury electric cars, the Zeekr 001 estate and the Zeekr X SUV, in the Netherlands and Sweden. The company plans to begin deliveries in the autumn, with prices starting at 59,490 euros for the Zeekr 01 and 44,990 euros for the Zeekr X.

What We’ve Been Reading This Month:

Pony.ai has launched a fully unmanned robotaxi service in Shenzhen, Guangdong province, following a cooperation framework agreement with local authorities. The project, based on regular fully unmanned operation, aims to cover core areas in Shenzhen and will not require a safety officer or driver to be present in the vehicle.

Ford will receive a conditional loan of $9.2 billion from The US Department of Energy to construct three large EV battery factories. This loan, is the largest government offering to an automaker since the 2009 bailouts. Ford plans to partner with SK Innovation to build the battery plants in Kentucky and Tennessee, with the goal of supplying enough capacity for 2 million EVs annually by 2026.

Electrify America, a subsidiary of Volkswagen, plans to incorporate Tesla’s NACS charging standard into its fast-charging networks in the United States and Canada by 2025, in addition to the existing Combined Charging System (CCS-1) connector.

General Motors Energy has introduced Ultium Home, a residential business unit offering energy management products. These products cater to bidirectional charging for GM EVs and stationary battery storage. GM Energy has also partnered with SunPower for solar energy integration.

General Motors announced its next-generation Ultra Cruise driver-assist system will feature lidar, along with other advanced sensors, to enable hands-free driving and cover 95% of driving maneuvers. The updated system will utilize cameras, short- and long-range radar, and a lidar sensor, with an all-new computer to process the sensor data.

Mercedes-Benz has received approval from California to use its Drive Pilot SAE Level 3 automated driving technology, making it the second state, after Nevada, to certify the system. The system will be available as an option for the 2024 Mercedes-Benz S-Class and EQS Sedan models in the US, allowing drivers to engage in secondary activities while the system controls the vehicle.

Porsche has partnered with Mobileye, Intel’s autonomous driving unit, to bring hands-free automated assistance and navigation functions to its upcoming models and potentially extend the technology to other brands within the Volkswagen Group. The collaboration will utilize Mobileye’s SuperVision technology platform to enable features such as autonomous lane changing and automatic overtaking.

Uber Technologies and Alphabet’s Waymo have announced a partnership to offer driverless cars on Uber’s ride-hailing and food delivery platform. Starting later this year, Uber customers in Phoenix, Arizona, will have access to a limited number of Waymo’s driverless vehicles for rides and deliveries within a designated area of 180 square miles.

WeRide, a Chinese start-up specializing in driverless vehicle development, has announced plans to allocate more resources to level 4 (L4) autonomous driving technology. This move by WeRide aligns with Beijing’s objective of reducing logistics costs and enhancing profitability for companies operating in the autonomous driving sector. WeRide has already deployed its autonomous bus, known as robobus, in 18 cities worldwide.

RoboSense, a provider of smart LiDAR sensor systems, joined force with NVIDIA Omniverse ecosystem to accelerate the development, testing, and validation of its sensor technology. The integration allows RoboSense’s second-generation smart solid-state LiDAR model to be integrated into NVIDIA DRIVE Sim, which is built on the Omniverse platform.

Magna International has completed the acquisition of Veoneer’s Active Safety business for a valuation of US$1.525 billion, solidifying its position as a key player in the ADAS and autonomous vehicle market. The deal expands Magna’s ADAS portfolio, adds engineering resources and software capabilities, and is expected to generate approximately US$3 billion in ADAS sales by 2024.

The content in this letter is for information illustration only. This website contains material sent to GLy Capital by third parties. GLy Capital is not responsible for any error, omission or inaccuracy in this material. GLy Capital reserves the right to omit, suspend or edit any material submitted. GLy Capital is not providing any investment advice or comment in this letter, and you should seek your own independent professional advice regarding any investment decision or advice. Unless otherwise stated, all copyright and other intellectual property rights in the materials on this letter belong to GLy Capital. Such materials may be downloaded or printed for personal use or for use within an individual firm or organisation but may only be used for personal viewing purposes or for viewing within that firm or organisation. Such materials may not be reproduced for or distributed to third parties, or used for commercial purposes, without GLy Capital’s prior written consent. Consent is not required where extracts of no more than a few relevant paragraphs are to be copied to third parties incidental to advice or other activities, provided that the source is properly acknowledged.