Clean hydrogen as a dependable and eco-friendly energy option is projected to lead to its market surpassing the value of liquid natural gas trade by 2030. This trend is anticipated to continue, potentially reaching a staggering annual value of US$1.4 trillion by 2050. Notably, the focus is on green hydrogen, which is generated through the electrolysis of water using renewable energy-driven electrical currents.

(Saman A Gorji, 2023)

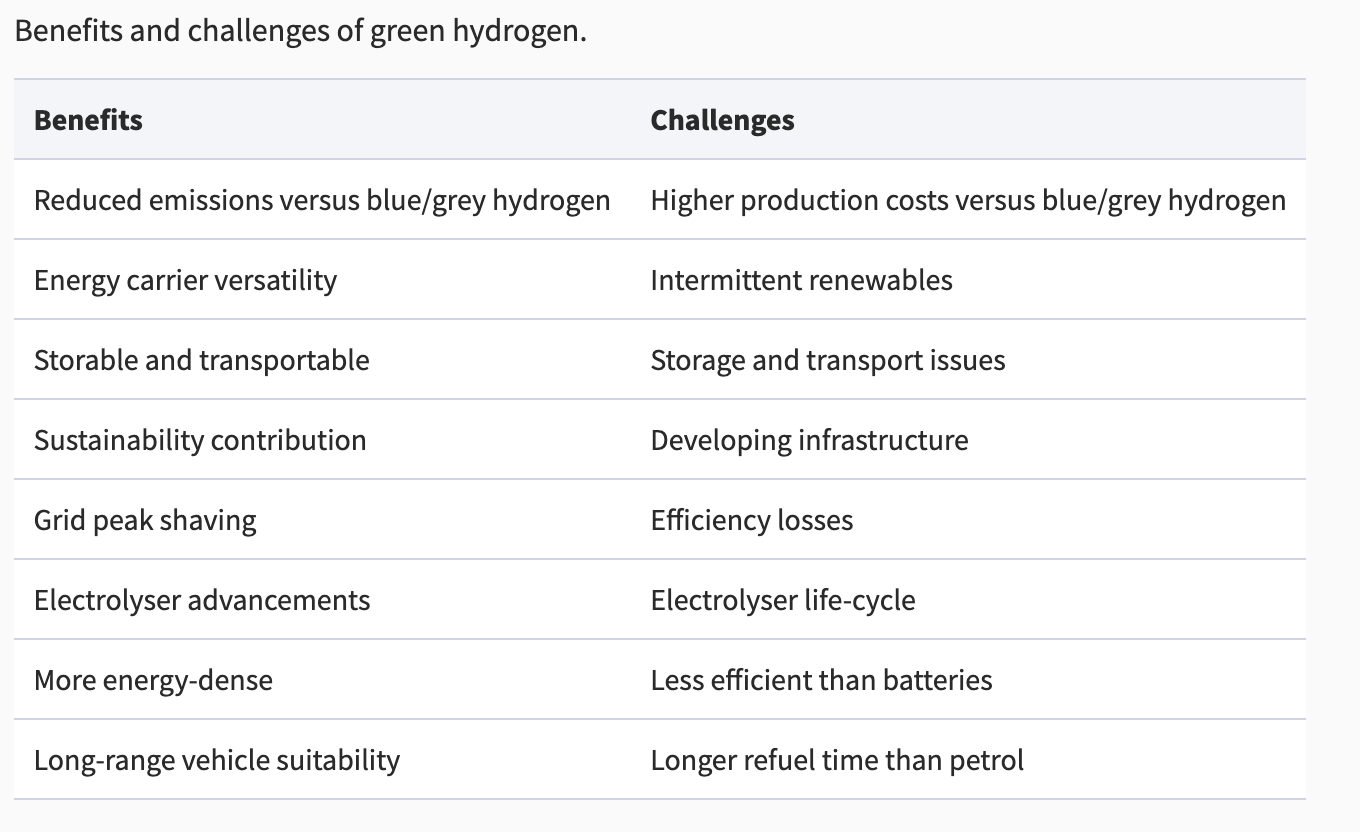

Green hydrogen, produced through electrolysis utilizing renewable energy sources, presents a cleaner substitute to conventional grey and blue hydrogen. This has the potential to significantly reshape the global energy landscape due to its reduced emissions, adaptability, and capacity for storage. While green hydrogen offers valuable benefits like decreased greenhouse gas emissions, energy transport capabilities, and extended storage options, it is not without challenges. These include higher production costs, intermittent renewable energy supply, and the necessity for efficient storage and transportation solutions.

In this context, the supply chain assumes a pivotal role in efficiently converting renewable energy into hydrogen, ensuring secure storage and seamless transportation, and enabling effective utilization. Despite this critical role, several challenges associated with production, storage, transportation, and consumption must be effectively addressed to fully unlock the potential of hydrogen, emphasizing the significance of optimization in the process. Presently, no single optimization technique is universally endorsed as the ultimate solution across diverse domains and industries. Each methodology has its own unique challenges.

For instance, exact methods, while robust, can be time-intensive and intricate to apply when dealing with optimal solutions for green hydrogen production within the supply chain. Additionally, the dynamic nature of energy systems further complicates the application of these algorithms, making the sustainability of obtained solutions uncertain. This complexity underscores the demand for inventive strategies and continuous research developments.

For the present discussion, we will focus specifically on the realm of green hydrogen production. But we take note that the value chain of green hydrogen is complex and capital intensive, encompassing production, storage, transportation, and consumption and many sub-segments that are yet developing.

Green Hydrogen Production:

Currently, the majority of hydrogen production is categorized as “gray,” originating from hydrocarbons like natural gas, a process known as steam reforming that emits carbon. “Blue” hydrogen also comes from hydrocarbons but incorporates carbon capture, utilization, and storage (CCUS) technology to reduce environmental effects, albeit with additional investments. On the other hand, “green” hydrogen is generated via renewable energy, particularly water electrolysis, and is emission-free.

Green hydrogen production hinges on water electrolysis powered by renewable sources like solar, wind, and hydropower. This transformative process disassembles water into hydrogen and oxygen using electric currents. Various electrolysis technologies—alkaline, proton exchange membrane (PEM), solid oxide, and anion exchange membrane (AEM)—offer distinct strengths and limitations.

Challenges and Current Landscape:

High Costs: Establishing green hydrogen facilities demands substantial investments in renewable energy infrastructure, electrolysis equipment, and system integration. Hydrogen production contends with substantial capital and operational expenses, impeding widespread adoption.

Moderate Efficiency: Current green hydrogen production methods exhibit limited efficiency, averaging around 30%, prompting the pursuit of technological enhancements.

Resource Limitations: Some regions face constraints due to scarce renewable energy sources and water resources, posing obstacles to scalable production. Varying operating conditions such as operating temperatures, pressures, and response times influences technology selection for specific applications and energy systems.

China’s Surge: The green hydrogen domain is experiencing a notable surge in China, where rapid developments are shaping the landscape. Notably, Gore holds a prominent position as the market leader in this context.

Strategic Imperative: The industry collectively grapples with the need to devise an effective and efficient approach for producing green hydrogen.

Leading Market Players: Several key players dominate the landscape, each contributing to the shaping of the industry’s trajectory. Noteworthy names include: Monolith, Sunfire, Electric Hydrogen, Enapter, ITM Power, Nel, Electrochaea

Factors to Attain Success:

The road to success in the green hydrogen realm is guided by essential factors that underpin sustainable growth:

Cost-Effective Energy Sources: Achieving the pivotal milestone of US$2 per kilogram for transportation applications and US$1 per kilogram for industrial and bulk power/polygeneration applications is instrumental in driving adoption, contrasting with the current range of US$5-6 per kilogram.

Efficient and Scalable Electrolysis Technology: The evolution of electrolysis technology toward scalability and efficiency significantly contributes to realizing green hydrogen’s potential.

Access to Resources: Uninterrupted access to water resources and robust infrastructure forms a foundation for viable production.

Presently, green hydrogen technology is in its fledgling stages and hasn’t undergone industrial-scale testing. In electrolysis-based hydrogen fuel production, electrons interact with water, leaving oxygen as a by-product. Only a minor 4% of current hydrogen production uses electrolysis due to its inefficiency and costliness compared to thermal combustion-based production. This implies that green hydrogen production remains pricier than coal or natural gas-based hydrogen production.

Going forward, innovative water electrolysis technologies are emerging, including waste heat recovery and solid-state electrolysers, aimed at enhancing efficiency and reducing costs. Further advancements are seen in the optimization of electrolyser systems through catalyst and membrane development, coupled with effective thermal management. Integrating these production methods with Direct Current (DC) microgrids demonstrates potential efficiency improvements, with PV panels, batteries, and electrolysers harmoniously operating as DC sources and loads. Moreover, the utilization of advanced materials like gallium nitride (GaN) and superconductors holds promise for more efficient power conversion processes.

Despite the complex challenges, the market for hydrogen remains robust, with more than 1,000 project proposals globally. Of these, 795 projects aim to be commissioned by 2030, representing USD 320 billion in direct investments. Europe takes the lead in proposed investments, with approximately 30%. North America and Latin America follow, each representing about 15% of announced investments, and China is spearheading the deployment of electrolyzers (200 MW). Japan and South Korea emerge as frontrunners in fuel cell manufacturing, collectively boasting over half of the world’s 11 GW manufacturing capacity. Giga-scale projects (requiring over 1 GW of electrolysis or more than 200,000 kt p.a. of low-carbon hydrogen) have almost doubled in number, indicating the strong industry momentum. However, to align with the net-zero target by 2050, investments must more than double by 2030.

GLy ecosystem update:

FreeWire recently introduced Mobilyze Pro, an AI-powered platform that aims to expand EV charging infrastructure efficiently. Leveraging AI tools like utilization prediction, tariff recommendation, and profitability calculation, Mobilyze Pro identifies optimal EV fast charging locations. With the need for extensive charging infrastructure to support the growing number of EVs, FreeWire’s platform assists site hosts in meeting demand by providing accurate forecasts and enabling informed decisions on hardware and site locations.

Polestar has achieved a significant production milestone by manufacturing 150,000 units of the Polestar 2 since its launch in China in 2020. The success of the Polestar 2, the brand’s inaugural all-electric vehicle, highlights the increasing global demand for sustainable cars. The brand’s unique research and development efforts have helped it gain traction, especially in the UK, where over 20,000 units were sold, marking a remarkable 174% growth in new registrations within the first seven months of 2023. This accomplishment underscores the brand’s significance in the European market, with the 100,000th Polestar 2 being delivered to a customer in Dublin, Ireland.

ECARX, Polestar and Mobileye have joined forces to introduce Mobileye’s Chauffeur autonomous driving technology in the upcoming Polestar 4, making it the first production car to feature this technology. The integration will be carried out by ECARX, and potential applications in future Polestar models are envisioned.

Dongfeng Peugeot-Citroën Automobile selects ECARX to build its next generation of intelligent cockpits. In collaboration with China Unicom Smart Connection (CUSC), ECARX has been selected by Dongfeng Peugeot-Citroën Automobile (DPCA) to provide Intelligent Cockpit 2.0 products based on the ECARX E02 intelligent cockpit computing module for three major vehicle launches this year. These products are integrated into DPCA’s new Citroën Tianyi, Peugeot 4008 compact SUV, and Peugeot 508L long-wheelbase sedan models, recently launched for mass production. The E02 module offers advanced features like data encryption, facial recognition, augmented reality navigation, and supports up to four independent displays, enhancing the driving experience and comfort for consumers.

Volvo Cars has unveiled a teaser for their upcoming all-electric model, the Volvo EM90, marking their first electric premium multi-purpose vehicle (MPV). This model is part of Volvo’s next-generation BEV lineup, following the Volvo EX90 and Volvo EX30. The EM90 is likely to be built upon the battery and powertrain configuration of the EX90, potentially featuring a battery capacity of over 100 kilowatt-hours and a range exceeding 300 miles.

What We’ve Been Reading This Month:

ElectraMeccanica is to merge with UK-based truck manufacturer Tevva, focusing on expanding their presence in the electric truck market. The move signifies a shift for ElectraMeccanica, which faced challenges with their Solo electric vehicle and decided to pivot towards medium- and heavy-duty commercial electric trucks. The merger aims to capitalize on the growing demand for electric trucks, utilizing ElectraMeccanica’s Mesa, Arizona plant to produce Tevva’s 7.5T model and enter markets in the UK, Europe, and the US.

The U.S. Department of Energy (DOE) has granted nearly $34 million to 19 research projects led by industry and universities to enhance the accessibility and affordability of clean hydrogen, facilitating its use in electricity generation, industrial decarbonization, and transportation. The funding supports the DOE’s Hydrogen Shot initiative, which strives to reduce clean hydrogen costs by 80% to $1 per kilogram within a decade, fostering new clean hydrogen pathways in the United States.

Arm, a chip design company owned by SoftBank, has filed for an initial public offering (IPO) on the Nasdaq exchange. This IPO is anticipated to be one of the largest in recent years and comes after Nvidia’s failed attempt to acquire Arm for $40 billion, following opposition from regulators and major chip companies. Arm, known for its energy-efficient microprocessor blueprints used in a wide range of products, including mobile phones and various devices, estimates that over 250 billion Arm-based chips have been sold.

Fourier Intelligence’s humanoid robot, GR-1, made an impressive debut at the World Artificial Intelligence Conference (WAIC) in Shanghai, showcasing the potential of bipedal robots. The GR-1 walked at 5 km/h on two legs while carrying a 50 kg load, drawing attention in the midst of AI software discussions. Originating as a rehabilitation robotics startup in 2015, Fourier Intelligence has expanded its portfolio to include various robotic devices, aligning with Elon Musk’s vision of humanoid robots assisting with everyday tasks. The company also acknowledges the potential of large language models (LLMs) like AI chatbots to enhance robots’ logical reasoning abilities.

Ford has partnered with SK On and EcoPro BM, South Korean battery manufacturers, to build a cathode manufacturing facility in Quebec with a $1.2 billion investment. This move is crucial for providing battery materials for Ford’s upcoming electric vehicles. The Inflation Reduction Act’s tax credits have spurred the growth of domestic battery factories in the U.S., prompting Ford to collaborate with SK On’s three battery cell manufacturing facilities with a combined capacity of 164 gigawatt-hours annually. To secure EV tax credits under the act, Ford is focusing on sourcing battery materials in alignment with specific production guidelines. Other automakers like General Motors and Tesla are also working to secure their battery material supply through investments and initiatives.

Renewable infrastructure investor Renewa, backed by investment manager QIC, has secured $450 million in committed capital to support its expansion in the U.S. renewable energy sector. The funding round, led by QIC, enables Renewa, based in Houston, Texas, to focus on obtaining land and leasing it to utility-scale renewable energy, storage, and other infrastructure projects. With ownership of land and ground leases in over 130 projects totaling more than 30 GW, Renewa boasts one of the largest independent portfolios of land under clean energy projects in the U.S., housing power plants operated by notable companies in 26 states.

The content in this letter is for information illustration only. This website contains material sent to GLy Capital by third parties. GLy Capital is not responsible for any error, omission or inaccuracy in this material. GLy Capital reserves the right to omit, suspend or edit any material submitted. GLy Capital is not providing any investment advice or comment in this letter, and you should seek your own independent professional advice regarding any investment decision or advice. Unless otherwise stated, all copyright and other intellectual property rights in the materials on this letter belong to GLy Capital. Such materials may be downloaded or printed for personal use or for use within an individual firm or organisation but may only be used for personal viewing purposes or for viewing within that firm or organisation. Such materials may not be reproduced for or distributed to third parties, or used for commercial purposes, without GLy Capital’s prior written consent. Consent is not required where extracts of no more than a few relevant paragraphs are to be copied to third parties incidental to advice or other activities, provided that the source is properly acknowledged.