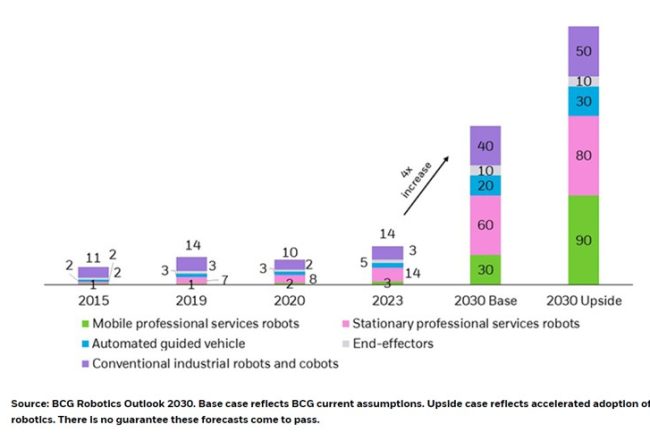

A convergence of factors is propelling the rise of robots into prominence, such as: wage inflation, persistent labor shortages, shifting demographic patterns, and the ongoing transformation of supply chains. These forces are reshaping industries and, in turn, fueling the demand for robotics.

The robotics sector can be categorized based on the following sectors and related sub-sector:

Industrial Applications:

- Traditional Industrial Robots: Including SCARA (Selective Compliance Assembly Robot Arm) embodying precision and efficiency in assembly and manufacturing processes.

- Robots AGV (Automatic Guided Vehicles): These autonomous vehicles navigate predefined paths in industrial environments, facilitating seamless material handling and logistics operations.

- AMR (Autonomous Mobile Robots): The epitome of warehouse automation, AMRs are revolutionizing logistics by enhancing order picking, inventory management, and overall operational efficiency.

- Collaborative Robots: Designed to work alongside humans, collaborative robots are cheaper than traditional industrial robots. Lightweight and human-friendly, they mainly serve small to medium manufacturing sites.

Service Robots:

- Humanoids: Robots designed in the likeness of humans. Current applications used in service industry, warehouse, healthcare, and education

- Home Service Robots: Including Robotic vacuum cleaners and smart home assistants

- Commercial Service Robots: In sectors like food delivery, hospitality and retail, expecting to register a CAGR of 33.65% from 2023 to 2028.

Technological Components:

- Hardware: Motion module and sensing module such as cameras and LiDAR.

- Software: Simulation and modelling used to test and validate robotic system before deployment. Perception and sensing, enabling robots to understand and interpret the environment through cameras and depth sensor.

- AI Chips: A range of specialized chips powering artificial intelligence algorithms such as GPU, ASIC, CiM and chiplets.

- Quantum Computing

For this discussion, we will specifically look into the industrial application sector. Amongst which, traditional industrial robots, AGV and collaborative robots are relatively stable and mature with established players and steady technological advancement. Comparatively, the sector of AMR highlights the immense growth potential for expansion, pricing pressures are expected to be balanced, ensuring a sustainable market trajectory.

Overview:

Autonomous Mobile Robots (AMRs) represent a significant evolution from the well-established Automated Guided Vehicles (AGVs) that have been utilized in factories since the 1950s. Both are two popular technologies used in industrial settings. What sets AMRs apart is their ability to operate independently and its flexibility to navigate unstructured environments. Equipped with advanced sensors, AMRs possess the capability to comprehend and interpret their surroundings, allowing them to efficiently navigate obstacles and unforeseen challenges, such as objects falling from shelves.

The global market for AMR technology is segmented into five key regions: North America, Europe, APAC, the MEA, and South America. In APAC, government initiatives promoting manufacturing automation, such as China’s “Made in China 2025” plan and India’s “Make in India” initiative, have been instrumental in driving AMR adoption. According to the latest research from Inkwood, the global AMR technology market is anticipated to reach $14.47 billion by 2030, at a CAGR of 21.31% from 2022 to 2030.

In 2022, APAC leads the market with a substantial 38% share and a robust 26.9% CAGR, poised to reach USD3.2 billion by 2030. Europe closely follows with a 35% market share, and North America holds a 26% share. Both the European and North American markets are driven by strong automotive sectors.

Compare to AGV, which is limited to pursuing pre-defined paths or using a set of waypoints, AMR operates autonomously in uncontrolled environments. Integrates sensors, actuators, and control systems, AMR can perceive their surroundings and make decisions based on the gathered data. The system employs simultaneous localization and mapping methods to determine the robot’s position and generate a map of the area, enabling the robot to navigate independently and avoid obstacles. Generally, AMR offer high adaptability at different locations with software configuration.

Currently, AMR technologies are applied in three main areas:

- AMR in Warehouse Management: for transporting materials and ensuring effective storage and distribution. AMR are equipped with advanced sensors and navigation systems, and can navigate warehouses and deliver items accurately. AMR carriers can also be incorporated with existing warehouse management systems for real-time material tracking.

- AMR in Logistics: In e-commerce for order fulfillment, enabling quick and efficient picking and packing of items for shipment; and in automating retail operations, such as restocking shelves. AMRs can also facilitate on-demand transportation of pallets between warehousing and manufacturing facilities.

- AMR in Manufacturing (Industrial Automation): For thorough product inspections, quality assessments, and predictive maintenance. AMRs can also be reprogrammed as automated guided vehicles, transporting raw materials and finished products within and between facilities.

Continuous advancements in automated assembly lines and AMR robot technology are poised to further transform the automotive manufacturing industry. The future holds highly automated factories, shorter production cycles, and higher-quality automotive products. This synergy between automated assembly lines and AMR robots can enable various tasks in material handling, parts supply, inventory management, and collaborative assembly.

It is expected that larger AMR companies will experience significant growth, while smaller entities are likely to be acquired by prominent manufacturers or logistics firms. For instance, after decade of the inception of Amazon Robotics, Amazon has unveiled its most advanced AMR yet — Proteus. Proteus stands out as the company’s inaugural robot labeled “fully autonomous”, which is designed to collaboratively work alongside human employees, moving packages within Amazon’s warehouses. Similarly, potential acquirers of smaller mobile robot enterprises include major automation conglomerates like Siemens or ABB, as well as companies such as Dematic or Honeywell, which specialize in automating warehouses for various clients.

Key Factors for the Success of AMR Technology:

Within the automotive domain, AMRs must offer economic viability in comparison to direct AGV deployment. Other success factor such as technological Advancements in sensor accuracy; battery management systems; hybrid models; locomotion and total energy consumption; path planning algorithms and scheduling methods for energy optimization; algorithm choice and design based on specific requirements and constraints.

Overall, fierce competition is relatively sparse. This can be attributed to distinct niches among AMR vendors, such as unique business models (i.e. Robotics-as-a-Service) and specialized problem-solving approaches within specific material handling processes. Each vendor addresses unique customer needs, leading to coexistence with minimal direct competition. Many AMR vendors emphasize the value of their solutions in software and workflow optimization, anticipating hardware commoditization. Consequently, the market is shifting towards subscription-based software models, with potential future pricing pressures influenced by evolving safety standards and the increasing adoption of SLAM-based technology, which raises the cost of robots. These factors are reshaping the industry dynamics, emphasizing the importance of software differentiation and the emergence of new challenges in pricing strategies.

GLy ecosystem update:

ECARX’s subsidiary, JiKa Automotive Electronics, has signed a strategic cooperation agreement with GYMD Digital Technology to construct JiKa Automotive Electronics’ intelligent factory. The collaboration will deploy GYMD’s smart factory construction solutions to create a digitally native enterprise-level smart factory integrating agile design, intelligent supply chain management and lean manufacturing.

Geely Holding Group and Baidu’s joint venture, Jidu Auto, has unveiled its first AI-powered electric vehicle, Ji Yue 01, priced from 249,900 yuan ($34,151.8). The SUV integrates Baidu’s Ernie Bot, a large language model, and has a range of 720 kilometers on a single charge.

Proton and Geely are contemplating the establishment of an electric vehicle plant in Thailand, according to Thai Prime Minister Srettha Thavisin. Following discussions with Malaysian leader Anwar Ibrahim, both sides plan to hold a meeting to determine the next steps. Geely, with a 49.9% stake in Proton, has been instrumental in revitalizing the Malaysian brand and expanding its presence in Southeast Asia.

Volvo Cars has partnered with Swedish wind power company Eolus Vind to power its Torslanda factory in western Sweden using a 1 gigawatt offshore wind farm, which will supply significant electricity to both the Torslanda factory and the new 50 GWh battery plant being built by Volvo Cars and Northvolt through their joint company Novo Energy. Construction is set to begin in 2027, with the wind farm coming online in 2029.

Volvo Cars has inaugurated its largest 22,000 square meters software test center in Gothenburg, Sweden, which is set to expand and double its capacity over time. The center will house 500 test benches and digital test environments.

Smart has signed a MoU with AW Rostamani Group, a leading automotive distributor in the UAE. As part of this collaboration, Smart plans to introduce its portfolio of all-electric vehicles in the UAE.

Renault plans to invest 3 billion euros by 2027 to launch eight new vehicles outside Europe as part of a global re-launch. The first of Renault’s new global vehicles is a small SUV named Kardian, derived from the Dacia Sandero, set to be launched next year in Latin America and Morocco. Five of the new models will be compact or larger, positioning the brand in lucrative market segments.

What We’ve Been Reading This Month:

Idemitsu Kosan and Toyota Motor Corporation have collaborated to develop mass production technology for solid electrolytes, enhance productivity, and establish a supply chain for all-solid-state batteries used in battery electric vehicles (BEVs). Both companies, leading in the field of material development for these batteries, aim to commercialize all-solid-state batteries in 2027-28, with the goal of achieving full-scale mass production.

Cruise has suspended all its driverless robotaxi operations across United States to “rebuild public trust.” This decision follows the suspension of Cruise’s robotaxi permit in California due to safety concerns raised by regulators, after the National Highway Traffic Safety Administration initiated an investigation into Cruise following reports of pedestrian injuries involving its driverless vehicles, including a notable incident in San Francisco where a woman was struck and pinned under a Cruise robotaxi.

Amazon has announced plans to begin testing Agility’s bipedal robot, Digit, in its fulfillment centers. The move is part of Amazon’s exploration of various robotic technologies for enhancing its operations. While the company’s main focus has been on wheeled autonomous mobile robots like those from Kiva Systems, Amazon Robotics is also interested in walking robots. The pilot with Digit will enable Amazon to assess the potential of legged locomotion in its warehouses and understand how it could enhance productivity and efficiency in different terrains.

General Motors and Honda have announced to halt their plan to jointly produce affordable EVs due to challenges including high interest rates and battery costs. The partnership, which aimed to develop affordable EVs priced under $30,000, was based on GM’s Ultium EV platform. Despite this setback, GM remains committed to producing lower-cost EVs, focusing on scaling the Ultium Platform and battery cell capacity. Meanwhile, GM and Honda are intensifying their efforts in the autonomous vehicle sector, planning to launch a robotaxi service in Japan using Cruise Origin vehicles in early 2026 under a new joint ventures.

GM has introduced “uServices,” a set of APIs for software developers, as part of its efforts to enhance the technology experience in its vehicles and extend the functionality to competitors’ vehicles. uServices functions as GM’s own API, enabling developers to create apps that work across various vehicle lineups. GM has also submitted this new definition to the Connected Vehicle Systems Alliance (COVESA), a global organization dedicated to developing open standards and technologies for connected vehicles.

China-based Zhipu AI has raised $342 million from investors including Alibaba, Tencent, Meituan, Xiaomi, Hillhouse, and Legend Capital. The startup, often compared to OpenAI, released a generative AI chatbot in August. With strong backing from major tech companies, Zhipu AI aims to lead an AI boom in China and contribute to the development of advanced artificial intelligence models.

Arenko has optimized its second battery co-located with a wind farm for Vattenfall, a major energy company. The battery features a 45.5 MWh Fluence battery system co-located alongside Vattenfall’s Ray 54.4 MW wind farm. Arenko’s Nimbus software integrates live wind generation predictions and live generation data from the wind farm to enable AI-driven optimization, allowing for precise control and dispatch of the battery. This achievement is a significant development for co-located renewable energy projects.

Stockholm plans to implement the first complete ban on gasoline and diesel-fueled cars in a commercial district of its downtown area by 2025. The ban, covering a 20-block zone, aims to reduce pollution, noise, and promote electric vehicle usage, making it a pioneering move among European capitals.

The EV startup WM Motor has filed for bankruptcy, confirmed by the Shanghai Third Intermediate People’s Court. The once-promising EV manufacturer faces challenging times, with limited details available about the circumstances leading to the bankruptcy. Earlier attempts to go public via a reverse takeover with Hong Kong-listed Apollo Future Mobility fell short, and recent developments, including the suspension of ownership transfer and potential acquisition by Kaixin Auto, have added complexity to the situation. WM Motor’s future in the competitive EV market remains uncertain.

The content in this letter is for information illustration only. This website contains material sent to GLy Capital by third parties. GLy Capital is not responsible for any error, omission or inaccuracy in this material. GLy Capital reserves the right to omit, suspend or edit any material submitted. GLy Capital is not providing any investment advice or comment in this letter, and you should seek your own independent professional advice regarding any investment decision or advice. Unless otherwise stated, all copyright and other intellectual property rights in the materials on this letter belong to GLy Capital. Such materials may be downloaded or printed for personal use or for use within an individual firm or organisation but may only be used for personal viewing purposes or for viewing within that firm or organisation. Such materials may not be reproduced for or distributed to third parties, or used for commercial purposes, without GLy Capital’s prior written consent. Consent is not required where extracts of no more than a few relevant paragraphs are to be copied to third parties incidental to advice or other activities, provided that the source is properly acknowledged.